Skip to content

Open Search Modal

Crypto Converter

News

Business

Crypto

Tech

Economy

Op-Ed

Regulation

Learn

Courses

Investing

NTF’s

Tech

Pulse Room

Deep-Dive

Industry Thoughts

Interviews

Research

Thought Leadership

Price Predictions

Newsletter

Open Search Modal

Crypto Converter

News

Crypto

Economy

Regulation

Business

Tech

Op-Ed

Learn

Courses

Investing

NFT’S

Tech

Pulse Room

Deep-Dive

Industry Thoughts

Interviews

Research

Thought Leadership

Price Predictions

Newsletter

Follow US

Binance

X

Instagram

LinkedIn

CoinMarketCap

Telegram

Facebook

YouTube

Home

/

News

News

Ethereum considers ‘Tapered Issuance Burn’ proposal as inflation solution

41 minutes ago

News

Telegram’s Durov dismisses App Store removal as Apple overreaction to extortionists

3 hours ago

News

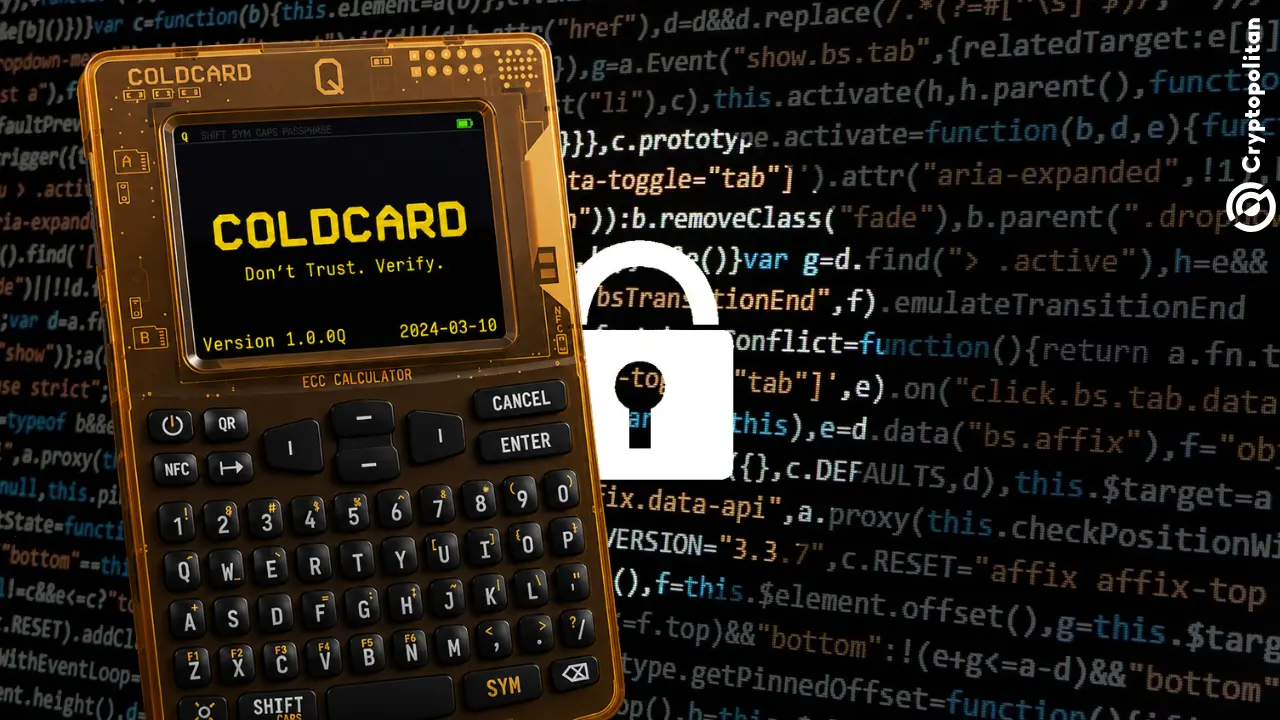

Coinkite CTO Peter Gray linked to the code behind the $114M Coldcard hack

5 hours ago

News

Nearly 70% of Russians see no use for crypto under Moscow’s new terms

7 hours ago

Regulation

US fourth-largest bank Wells Fargo plans fall launch of tokenized deposits service

7 hours ago

News

Sequans cuts Bitcoin stash to 314 coins as it clears debt and refocuses on chips

8 hours ago

News

live news & hot discussions

TUNE INTO

The loudest crypto insights in real time

US drafts ban on Chinese data center parts as AI feud with China widens

10 hours ago

Tech

China’s exoskeleton sales hit a record as robotic legs join its physical-AI push

10 hours ago

Tech

OpenAI calls out ‘oddly personal’ Apple for ‘careless, aggressive’ lawsuit

11 hours ago

Tech

Polosukhin floats NEAR sovereign fund to wean network from inflation

11 hours ago

News

Warren and Blumenthal press SEC to probe Trump memecoin as a ‘rug pull’

11 hours ago

News

Another Chinese startup AI² Robotics weighs Hong Kong IPO

11 hours ago

Tech

LIVE: Watch SpaceX report earnings for the first time since IPO

13 hours ago

Live Updates

Ether whales are pulling ETH off exchanges, Here’s why

15 hours ago

News

BEST COINS'26

TON

Explore

z

ZEC

Explore

BTC

Explore

Dogecoin (DOGE)

DOGE

Explore

HYPE

Explore

Peter Thiel’s Palantir surges after crushing earnings and raising its full-year forecast

23 hours ago

Business

Bitcoin’s next bottom may not arrive until late 2026

August 3, 2026

News

White House calls OpenAI, Google, Meta and Anthropic to AI safety-test talks

August 3, 2026

Regulation

Bessent’s crypto adviser leaves Treasury role to return in private sector return

August 3, 2026

News

BubbleMaps: CATE’s 20% supply concentration risk puts ‘DOGE sister’ on watchlist

August 3, 2026

News

Kenya chooses Avalanche as KNEC migrates education records on-chain

August 3, 2026

News

Strive, American Bitcoin, Bitmine buy as Strategy sells 1,638 BTC

August 3, 2026

News

Robinhood joins UK crypto register weeks before 2027 licensing window opens

August 3, 2026

Regulation

Posts navigation

1

2

3

4

…

3,461

Next

Stay ahead in crypto

One sharp brief.

Every day.

SUBSCRIBE